As filed with the Securities and Exchange Commission on October 30, 2025

Registration No. 333-

Registration of securities, business combinations

October 30, 2025

Published on October 30, 2025

|

|

|

|

|

|

|

|

|

Switzerland

|

|

|

3241

|

|

|

98-1807904

|

|

Delaware

|

|

|

3241

|

|

|

81-3818857

|

|

(State or other jurisdiction of

incorporation or organization)

|

|

|

(Primary Standard Industrial

Classification Code Number)

|

|

|

(I.R.S. Employer Identification No.)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Amrize Ltd

Grafenauweg 8

6300 Zug, Switzerland 6300

+41 41 562 34 90

|

|

|

Amrize Finance US LLC

8700 W. Bryn Mawr Ave.

Chicago, IL 60631

+41 41 562 34 90

|

|

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

|

|

|

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

|

|

|

|

|

|

|

|

|

|

|

|

Denise Singleton

Chief Legal Officer and Corporate Secretary

8700 W. Bryn Mawr Ave.

Chicago, IL 60631

+41 41 562 34 90

|

|

|

Hans Weinburger VP, Chief Securities & Finance Counsel

and Assistant Corporate Secretary

8700 W. Bryn Mawr Ave.

Chicago, IL 60631

+41 41 562 34 90

|

|

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

|

|

|

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Large accelerated filer

|

|

|

☐

|

|

|

Accelerated filer

|

|

|

☐

|

|

|

Large accelerated filer

|

|

|

☐

|

|

|

Accelerated filer

|

|

|

☐

|

|

|

|

|

☒

|

|

|

Smaller reporting company

|

|

|

|

|

|

|

|

|

☒

|

|

|

Smaller reporting company

|

|

|

|

|

|

|

|

|

|

|

Emerging growth company

|

|

|

|

|

|

|

|

|

|

|

|

Emerging growth company

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

•

|

We are offering to exchange up to:

|

|

○

|

$325,866,000 of our outstanding 3.500% Senior Notes due 2026 (the “2026 initial notes”) for a

like amount of our registered 3.500% Senior Notes due 2026 (the “2026 exchange notes” and, together with the 2026 initial notes, the “2026 notes”);

|

|

○

|

$700,000,000 of our outstanding 4.600% Senior Notes due 2027 (the “2027 initial notes”) for a

like amount of our registered 4.600% Senior Notes due 2027 (the “2027 exchange notes” and, together with the 2027 initial notes, the “2027 notes”);

|

|

○

|

$700,000,000 of our outstanding 4.700% Senior Notes due 2028 (the “2028 initial notes”) for a

like amount of our registered 4.700% Senior Notes due 2028 (the “2028 exchange notes” and, together with the 2028 initial notes, the “2028 notes”);

|

|

○

|

$1,000,000,000 of our outstanding 4.950% Senior Notes due 2030 (the “2030 initial notes”) for

a like amount of our registered 4.950% Senior Notes due 2030 (the “2030 exchange notes” and, together with the 2030 initial notes, the “2030 notes”);

|

|

○

|

$50,000,000 of our outstanding 4.200% Senior Notes due 2033 (the “2033 initial notes”) for a

like amount of our registered 4.200% Senior Notes due 2033 (the “2033 exchange notes” and, together with the 2033 initial notes, the “2033 notes”);

|

|

○

|

$1,000,000,000 of our outstanding 5.400% Senior Notes due 2035 (the “2035 initial notes”) for

a like amount of our registered 5.400% Senior Notes due 2035 (the “2035 exchange notes” and, together with the 2035 initial notes, the “2035 notes”);

|

|

○

|

$444,530,000 of our outstanding 7.125% Senior Notes due 2036 (the “2036 initial notes”) for a

like amount of our registered 7.125% Senior Notes due 2036 (the “2036 exchange notes” and, together with the 2036 initial notes, the “2036 notes”);

|

|

○

|

$191,348,000 of our outstanding 6.875% Senior Notes due 2039 (the “2039 initial notes”) for a

like amount of our registered 6.875% Senior Notes due 2039 (the “2039 exchange notes” and, together with the 2039 initial notes, the “2039 notes”);

|

|

○

|

$238,925,000 of our outstanding 6.500% Senior Notes due 2043 (the “2043 initial notes”) for a

like amount of our registered 6.500% Senior Notes due 2043 (the “2043 exchange notes” and, together with the 2043 initial notes, the “2043 notes”); and

|

|

○

|

$553,505,000 of our outstanding 4.750% Senior Notes due 2046 (the “2046 initial notes”) for a

like amount of our registered 4.750% Senior Notes due 2046 (the “2046 exchange notes” and, together with the 2046 initial notes, the “2046 notes”).

|

|

•

|

The term “exchange notes” refers collectively to the 2026 exchange notes, 2027 exchange notes, 2028 exchange notes, 2030

exchange notes, 2033 exchange notes, 2035 exchange notes, 2036 exchange notes, 2039 exchange notes, 2043 exchange notes and 2046 exchange notes. The term “initial notes” refers collectively to the 2026 initial notes, 2027 initial notes,

2028 initial notes, 2030 initial notes, 2033 initial notes, 2035 initial notes, 2036 initial notes, 2039 initial notes, 2043 initial notes and 2046 initial notes. The term “notes” refers to both exchange notes and initial notes.

|

|

•

|

We are making the exchange offers to satisfy your registration rights, as a holder of the initial notes, pursuant to

registration rights agreements that we entered into in connection with the issuance of the initial notes.

|

|

•

|

Each exchange offer will expire at 5:00 p.m., New York City time, on 2025, unless extended.

|

|

•

|

If all the conditions to an exchange offer are satisfied, we will exchange all of our relevant initial notes that are validly

tendered and not withdrawn in such exchange offer for the relevant exchange notes.

|

|

•

|

You may withdraw your tender of initial notes at any time before the expiration of the relevant exchange offer.

|

|

•

|

The exchange notes that we will issue you in exchange for your initial notes will be substantially identical to your initial

notes except that, unlike your initial notes, the exchange notes will have no transfer restrictions or registration rights.

|

|

•

|

The exchange notes that we will issue you in exchange for your initial notes are new securities with no established market

for trading.

|

|

•

|

The 2026 exchange notes will mature on September 22, 2026. Interest on the 2026 exchange notes will accrue at the rate of

3.500% per annum. We will pay interest on the 2026 exchange notes semi-annually in arrears on March 22 and September 22 of each year, commencing on March 22, 2026, to the holders of record of the 2026 exchange notes at the close of

business on March 8 or September 8, as the case may be, immediately preceding the relevant interest payment date.

|

|

•

|

The 2027 exchange notes will mature on April 7, 2027. Interest on the 2027 exchange notes will accrue at the rate of 4.600%

per annum. We will pay interest on the 2027 exchange notes semi-annually in arrears on April 7 and October 7 of each year, commencing on April 7, 2026, to the holders of record of the 2027 exchange notes at the close of business on

March 24 or September 23, as the case may be, immediately preceding the relevant interest payment date.

|

|

•

|

The 2028 exchange notes will mature on April 7, 2028. Interest on the 2028 exchange notes will accrue at the rate of 4.700%

per annum. We will pay interest on the 2028 exchange notes semi-annually in arrears on April 7 and October 7 of each year, commencing on April 7, 2026, to the holders of record of the 2028 exchange notes at the close of business on

March 24 or September 23, as the case may be, immediately preceding the relevant interest payment date.

|

|

•

|

The 2030 exchange notes will mature on April 7, 2030. Interest on the 2030 exchange notes will accrue at the rate of 4.950%

per annum. We will pay interest on the 2030 exchange notes semi-annually in arrears on April 7 and October 7 of each year, commencing on April 7, 2026, to the holders of record of the 2028 exchange notes at the close of business on

March 24 or September 23, as the case may be, immediately preceding the relevant interest payment date.

|

|

•

|

The 2033 exchange notes will mature on June 3, 2033. Interest on the 2033 exchange notes will accrue at the rate of 4.200%

per annum. We will pay interest on the 2033 exchange notes annually in arrears on June 3 of each year, commencing on June 3, 3026, to the holders of record of the 2033 exchange notes at the close of business on May 20 immediately

preceding the relevant interest payment date.

|

|

•

|

The 2035 exchange notes will mature on April 7, 2035. Interest on the 2035 exchange notes will accrue at the rate of 5.400%

per annum. We will pay interest on the 2035 exchange notes semi-annually in arrears on April 7 and October 7 of each year, commencing on April 7, 2026, to the holders of record of the 2035 exchange notes at the close of business on

March 24 or September 23, as the case may be, immediately preceding the relevant interest payment date.

|

|

•

|

The 2036 exchange notes will mature on July 15, 2036. Interest on the 2036 exchange notes will accrue at the rate of 7.125%

per annum. We will pay interest on the 2036 exchange notes semi-annually in arrears on January 15 and July 15 of each year, commencing on January 15, 2026, to the holders of record of the 2036 exchange notes at the close of business on

January 1 or July 1, as the case may be, immediately preceding the relevant interest payment date.

|

|

•

|

The 2039 exchange notes will mature on September 29, 2039. Interest on the 2039 exchange notes will accrue at the rate of

6.875% per annum, subject to the 2039 rate adjustment (as further described herein). We will pay interest on the 2039 exchange notes semi-annually in arrears on March 29 and September 29 of each year, commencing on March 29, 2026, to

the holders of record of the 2039 exchange notes at the close of business on March 15 or September 15, as the case may be, immediately preceding the relevant interest payment date.

|

|

•

|

The 2043 exchange notes will mature on September 12, 2043. Interest on the 2043 exchange notes will accrue at the rate of

6.500% per annum. We will pay interest on the 2043 exchange notes semi-annually in arrears on March 12 and September 12 of each year, commencing on March 12, 2026, to the holders of record of the 2043 exchange notes at the close of

business on the date that is the fifteenth calendar day immediately preceding the relevant interest payment date.

|

|

•

|

The 2046 exchange notes will mature on September 22, 2046. Interest on the 2046 exchange notes will accrue at the rate of

4.750% per annum. We will pay interest on the 2046 exchange notes semi-annually in arrears on March 22 and September 22 of each year, commencing on March 22, 2026, to the holders of record of the 2046 exchange notes at the close of

business on March 8 or September 8, as the case may be, immediately preceding the relevant interest payment date.

|

|

•

|

The exchange notes will be our senior unsecured obligations and rank pari passu in right of payment to all of our other

senior unsecured indebtedness and senior in right of payment to our subordinated indebtedness.

|

|

•

|

The exchange notes will be effectively subordinated to all of our secured indebtedness to the extent of the value of the

property or assets securing such indebtedness.

|

|

•

|

The exchange notes will be structurally subordinated to all obligations of our subsidiaries (including secured and unsecured

obligations).

|

|

|

|

|

|

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

|

|

|

(i)

|

“Amrize,” “we,” “us” and “our” refer to (i) the Amrize Business prior to the Spin-off as a carve-out business of Holcim and

(ii) the Company and its subsidiaries following the Spin-off;

|

|

(ii)

|

“Amrize Business” refers to the business, activities and operations of Holcim and its affiliates in the United States, Canada

and Jamaica (the “Amrize Territories”), including the manufacturing of cement, aggregates, ready-mix concrete, asphalt, roofing systems and other building solutions in the Amrize Territories, as well as certain support operations in

Colombia and certain trading operations;

|

|

(iii)

|

the “Board of Directors” or “the Board” refers to the board of directors of the Company;

|

|

(iv)

|

the “Company” refers to Amrize Ltd, incorporated in Switzerland with limited liability;

|

|

(v)

|

“Holcim” refers to Holcim Ltd and its consolidated subsidiaries (including Amrize for the period prior to the Spin-off);

|

|

(vi)

|

the “Holcim Board” refers to the board of directors of Holcim;

|

|

(vii)

|

the “issuer” refers to Amrize Finance US LLC, a Delaware limited liability company and a wholly-owned subsidiary of the

Company; and

|

|

(viii)

|

the “Spin-Off” refers to the transaction in which Holcim Ltd distributed to its stockholders 100% of the shares of the

Company’s common stock.

|

|

•

|

the non-Swiss court where the decision was rendered had jurisdiction pursuant to the Swiss Federal Act on Private

International Law;

|

|

•

|

the judgment of such non-Swiss court is no longer subject to any ordinary appeal or has become final;

|

|

•

|

the judgment does not contravene Swiss public policy;

|

|

•

|

the court procedures and the service of documents leading to the judgment were in accordance with the due process of law; and

|

|

•

|

no proceeding involving the same position and the same subject matter was first brought in Switzerland, or adjudicated in

Switzerland, or was earlier adjudicated in a third state and this decision is recognizable in Switzerland.

|

|

•

|

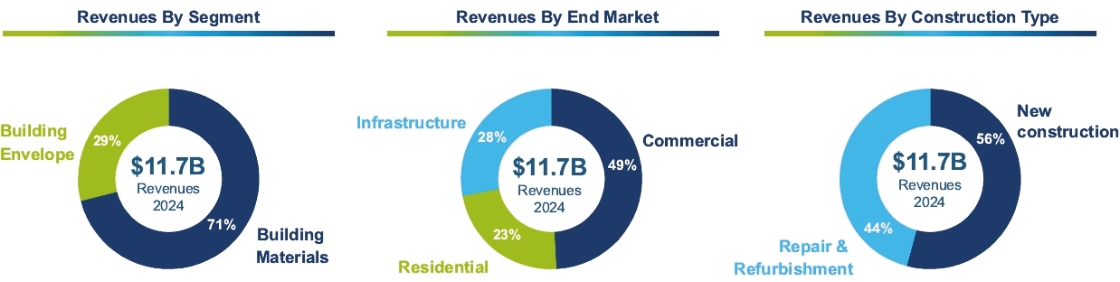

Our Building Materials segment offers a range of branded solutions delivering high-quality products for a wide range of

applications across North America. Key product offerings of this segment include cement and aggregates, as well as a variety of downstream products and solutions such as ready-mix concrete, asphalt and other construction materials.

|

|

•

|

Our Building Envelope segment offers advanced roofing and wall systems, including single-ply membranes, insulation,

shingles, sheathing, waterproofing and protective coatings, along with adhesives, tapes and sealants that are critical to the application of roofing and wall systems. Our Building Envelope products are sold individually or in

warranted systems for new construction or R&R in commercial and residential projects. These products are sold either directly to contractors or through an authorized distributor or dealer network in North America.

|

|

•

|

Economic conditions, including inflation, have affected and may continue to adversely affect our business, financial

condition, liquidity and results of operations.

|

|

•

|

We are affected by the level of demand in the construction industry.

|

|

•

|

We and our customers participate in cyclical industries and regional markets, which are subject to industry downturns.

|

|

•

|

Changes in the cost and/or availability of raw materials required to run our business, including related supply chain

disruptions, could have a material adverse effect on our business, financial condition and results of operations.

|

|

•

|

High energy and fuel costs have had and may continue to have a material adverse effect on our operating results.

|

|

•

|

The development and introduction of new products and technologies, or the failure to do so, could have a material adverse

effect on our business, financial condition, liquidity and results of operations.

|

|

•

|

We operate in a highly competitive industry with numerous players employing different competitive strategies and if we do

not compete effectively, our revenues, market share and results of operations may be adversely affected.

|

|

•

|

Activities in our business can be hazardous and can cause injury to people or damage to property in certain circumstances.

|

|

•

|

We are subject to the laws and regulations of the countries where we operate and do business and non-compliance, any

material changes in such laws and regulations and/or any significant delays in assessing the impact and/or adapting to such changes in laws and regulations may have an adverse effect on our business, financial condition, liquidity and

results of operations.

|

|

•

|

We or our third-party suppliers may fail to maintain, obtain or renew or may experience material delays in obtaining

requisite governmental or other approvals, licenses and permits for the conduct of our business.

|

|

•

|

We may not achieve some or all of the expected benefits of the Spin-off, and the Spin-off may adversely impact our

business.

|

|

•

|

The non-recurring and recurring costs of the Spin-off may be greater than we expected.

|

|

•

|

We have minimal history operating as an independent, publicly traded company, and our financial information in this

prospectus is not necessarily representative of the results that we would have achieved as a separate, publicly traded company and therefore may not be a reliable indicator of our future results.

|

|

•

|

There are currently no markets for the exchange notes, and active trading markets may not develop for the notes.

|

|

•

|

The initial notes are, and the exchange notes will be, unsecured and therefore will be effectively subordinated to the

issuer’s and the guarantor’s future secured debt.

|

|

•

|

As the guarantor is a holding company, its obligations under its guarantee will be structurally subordinated to liabilities

of its subsidiaries.

|

|

•

|

The issuance of the exchange notes may adversely affect the market for the initial notes.

|

|

•

|

Some persons who participate in the exchange offers must deliver a prospectus in connection with resales of the exchange

notes.

|

|

•

|

the exchange notes have been registered under the Securities Act of 1933, as amended (the “Securities Act”) and will be

freely tradable by persons who are not affiliated with us;

|

|

•

|

the exchange notes are not entitled to registration rights which are applicable to the initial notes under the relevant

registration rights agreement; and

|

|

•

|

our obligation to pay additional interest on the initial notes due to the failure to consummate the exchange offers by a

prior date does not apply to the exchange notes.

|

|

•

|

Up to $325,866,000 of 2026 exchange notes for a like aggregate principal amount of 2026 initial notes;

|

|

•

|

Up to $700,000,000 of 2027 exchange notes for a like aggregate principal amount of 2027 initial notes;

|

|

•

|

Up to $700,000,000 of 2028 exchange notes for a like aggregate principal amount of 2028 initial notes;

|

|

•

|

Up to $1,000,000,000 of 2030 exchange notes for a like aggregate principal amount of 2030 initial notes;

|

|

•

|

Up to $50,000,000 of 2033 exchange notes for a like aggregate principal amount of 2033 initial notes;

|

|

•

|

Up to $1,000,000,000 of 2035 exchange notes for a like aggregate principal amount of 2035 initial notes;

|

|

•

|

Up to $444,530,000 of 2036 exchange notes for a like aggregate principal amount of 2036 initial notes;

|

|

•

|

Up to $191,348,000 of 2039 exchange notes for a like aggregate principal amount of 2039 initial notes;

|

|

•

|

Up to $238,925,000 of 2043 exchange notes for a like aggregate principal amount of 2043 initial notes; and

|

|

•

|

Up to $553,505,000 of 2046 exchange notes for a like aggregate principal amount of 2046 initial notes.

|

|

•

|

there is no change in the laws and regulations which would impair our ability to proceed with such exchange offer;

|

|

•

|

there is no change in the current interpretation of the staff of the Securities and Exchange Commission (the “SEC”)

permitting resales of the exchange notes for such exchange offer;

|

|

•

|

there is no action or proceeding or threatened action or proceeding which would impair our ability to proceed with such

exchange offer;

|

|

•

|

we obtain all the governmental approvals we deem necessary to complete such exchange offer;

|

|

•

|

the customary representations, and any other representations as may be reasonably necessary under applicable SEC rules, of

the holders of the initial notes are accurate;

|

|

•

|

the holders of the initial notes satisfy customary conditions relating to the delivery of the initial notes; and

|

|

•

|

the holders of the initial notes execute and deliver customary documentation relating to the exchange offer.

|

|

•

|

except as set forth in the next paragraph, you will not necessarily be able to require us to register your initial notes

under the Securities Act;

|

|

•

|

you will not be able to resell, offer to resell or otherwise transfer your initial notes unless they are registered under

the Securities Act or unless you resell, offer to resell or otherwise transfer them under an exemption from the registration requirements of, or in a transaction not subject to, the Securities Act; and

|

|

•

|

the trading market for your initial notes will become more limited to the extent other holders of initial notes participate

in the exchange offers.

|

|

•

|

an initial purchaser requests us to register initial notes that are not eligible to be exchanged for exchange notes in the

applicable exchange offer;

|

|

•

|

you are not eligible to participate in the exchange offers;

|

|

•

|

you may not resell the exchange notes you acquire in the exchange offers to the public without delivering a prospectus and

that the prospectus contained in the exchange offer registration statement is not appropriate or available for such resales by you; or

|

|

•

|

you are a broker-dealer and hold initial notes that are part of an unsold allotment from the original sale of the initial

notes.

|

|

•

|

you are authorized to tender the initial notes and to acquire exchange notes, and that we will acquire good and

unencumbered title thereto;

|

|

•

|

the exchange notes acquired by you are being acquired in the ordinary course of business;

|

|

•

|

you have no arrangement or understanding with any person to participate in a distribution of the exchange notes and are not

participating in, and do not intend to participate in, the distribution of such exchange notes;

|

|

•

|

you are not an “affiliate,” as defined in Rule 405 under the Securities Act, of ours, or you will comply with the

registration and prospectus delivery requirements of the Securities Act to the extent applicable;

|

|

•

|

if you are not a broker-dealer, you are not engaging in, and do not intend to engage in, a distribution of exchange notes;

and

|

|

•

|

if you are a broker-dealer, initial notes to be exchanged were acquired by you as a result of market-making or other

trading activities and you will deliver a prospectus in connection with any resale, offer to resell or other transfer of such exchange notes.

|

|

•

|

2026 exchange notes: $325,866,000 aggregate principal amount;

|

|

•

|

2027 exchange notes: $700,000,000 aggregate principal amount;

|

|

•

|

2028 exchange notes: $700,000,000 aggregate principal amount;

|

|

•

|

2030 exchange notes: $1,000,000,000 aggregate principal amount;

|

|

•

|

2033 exchange notes: $50,000,000 aggregate principal amount;

|

|

•

|

2035 exchange notes: $1,000,000,000 aggregate principal amount;

|

|

•

|

2036 exchange notes: $444,530,000 aggregate principal amount;

|

|

•

|

2039 exchange notes: $191,348,000 aggregate principal amount;

|

|

•

|

2043 exchange notes: $238,925,000 aggregate principal amount; and

|

|

•

|

2046 exchange notes: $553,505,000 aggregate principal amount.

|

|

•

|

the Company had $5,264 million of total long-term debt (including current portion) on a consolidated basis, substantially

all of which constituted senior unsecured indebtedness and are obligations of the issuer;

|

|

•

|

the Company’s subsidiaries, including the issuer, had in the aggregate $5,811 million in total debt;

|

|

•

|

the Company had $11,137 million of total liabilities on a consolidated basis (including the initial notes); and

|

|

•

|

neither the Company nor the issuer had any secured indebtedness to which the exchange notes would be effectively junior.

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

Pro Forma

|

|

|

Historical

|

|||||||||||||||||||||

|

(In millions, except per share data)

|

|

|

Nine Months

Ended

September 30,

|

|

|

Fiscal Year

Ended

December 31,

|

|

|

Three Months

Ended

September 30,

|

|

|

Nine Months

Ended

September 30,

|

|

|

Fiscal Year Ended

December 31,

|

||||||||||||

|

|

2025

|

|

|

2024

|

|

|

2025

|

|

|

2024

|

|

|

2025

|

|

|

2024

|

|

|

2024

|

|

|

2023

|

|

|

2022

|

||

|

|

(Unaudited)

|

|

|

(Unaudited)

|

|

|

(Unaudited)

|

|

|

(Audited)

|

|||||||||||||||||

|

Revenues

|

|

|

$8,976

|

|

|

$11,704

|

|

|

$3,675

|

|

|

$3,446

|

|

|

$8,976

|

|

|

$8,855

|

|

|

$11,704

|

|

|

$11,677

|

|

|

$10,726

|

|

Cost of revenues

|

|

|

(6,702)

|

|

|

(8,634)

|

|

|

(2,589)

|

|

|

(2,404)

|

|

|

(6,702)

|

|

|

(6,562)

|

|

|

(8,634)

|

|

|

(8,908)

|

|

|

(8,254)

|

|

Gross profit

|

|

|

2,274

|

|

|

3,070

|

|

|

1,086

|

|

|

1,042

|

|

|

2,274

|

|

|

2,293

|

|

|

3,070

|

|

|

2,769

|

|

|

2,472

|

|

Selling, general and administrative expenses

|

|

|

(858)

|

|

|

(957)

|

|

|

(312)

|

|

|

(241)

|

|

|

(850)

|

|

|

(682)

|

|

|

(944)

|

|

|

(898)

|

|

|

(752)

|

|

Gain on disposal of long-lived assets

|

|

|

9

|

|

|

71

|

|

|

4

|

|

|

43

|

|

|

9

|

|

|

49

|

|

|

71

|

|

|

32

|

|

|

36

|

|

Loss on impairments

|

|

|

(2)

|

|

|

(2)

|

|

|

—

|

|

|

—

|

|

|

(2)

|

|

|

(2)

|

|

|

(2)

|

|

|

(15)

|

|

|

(57)

|

|

Operating income

|

|

|

1,423

|

|

|

2,182

|

|

|

778

|

|

|

844

|

|

|

1,431

|

|

|

1,658

|

|

|

2,195

|

|

|

1,888

|

|

|

1,699

|

|

Interest expense, net

|

|

|

(231)

|

|

|

(307)

|

|

|

(89)

|

|

|

(130)

|

|

|

(328)

|

|

|

(384)

|

|

|

(512)

|

|

|

(549)

|

|

|

(248)

|

|

Other non-operating income (expense), net

|

|

|

2

|

|

|

(55)

|

|

|

—

|

|

|

(11)

|

|

|

2

|

|

|

(7)

|

|

|

(55)

|

|

|

(36)

|

|

|

9

|

|

Income before income tax expense and income from

equity method investments

|

|

|

1,194

|

|

|

1,820

|

|

|

689

|

|

|

703

|

|

|

1,105

|

|

|

1,267

|

|

|

1,628

|

|

|

1,303

|

|

|

1,460

|

|

Income tax expense

|

|

|

(248)

|

|

|

(415)

|

|

|

(150)

|

|

|

(155)

|

|

|

(226)

|

|

|

(293)

|

|

|

(368)

|

|

|

(361)

|

|

|

(366)

|

|

Income from equity method investments

|

|

|

5

|

|

|

13

|

|

|

4

|

|

|

4

|

|

|

5

|

|

|

7

|

|

|

13

|

|

|

13

|

|

|

13

|

|

Net income

|

|

|

951

|

|

|

1,418

|

|

|

543

|

|

|

552

|

|

|

884

|

|

|

981

|

|

|

1,273

|

|

|

955

|

|

|

1,107

|

|

Net loss attributable to noncontrolling interests

|

|

|

3

|

|

|

1

|

|

|

2

|

|

|

1

|

|

|

3

|

|

|

2

|

|

|

1

|

|

|

1

|

|

|

1

|

|

Net income attributable to the Company

|

|

|

954

|

|

|

$1,419

|

|

|

$545

|

|

|

$553

|

|

|

$887

|

|

|

$983

|

|

|

$1,274

|

|

|

$956

|

|

|

$1,108

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

Pro Forma

|

|

|

Historical

|

|||||||||||||||||||||

|

(In millions, except per share data)

|

|

|

Nine Months

Ended

September 30,

|

|

|

Fiscal Year

Ended

December 31,

|

|

|

Three Months

Ended

September 30,

|

|

|

Nine Months

Ended

September 30,

|

|

|

Fiscal Year Ended

December 31,

|

||||||||||||

|

|

2025

|

|

|

2024

|

|

|

2025

|

|

|

2024

|

|

|

2025

|

|

|

2024

|

|

|

2024

|

|

|

2023

|

|

|

2022

|

||

|

|

(Unaudited)

|

|

|

(Unaudited)

|

|

|

(Unaudited)

|

|

|

(Audited)

|

|||||||||||||||||

|

Unaudited pro forma earnings per Company Share:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

|

|

|

$1.72

|

|

|

$2.57

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Diluted

|

|

|

$1.72

|

|

|

$2.57

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted-average number of Company Shares

outstanding:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

|

|

|

553.1

|

|

|

553.1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Diluted

|

|

|

553.3

|

|

|

553.1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

Historical

|

||||||

|

(In millions)

|

|

|

As of

September 30,

|

|

|

As of December 31,

|

|||

|

|

2025

|

|

|

2024

|

|

|

2023

|

||

|

|

(Unaudited)

|

|

|

(Audited)

|

|||||

|

Cash and cash equivalents

|

|

|

$826

|

|

|

$1,585

|

|

|

$1,107

|

|

Total assets

|

|

|

$24,035

|

|

|

$23,805

|

|

|

$23,047

|

|

Total liabilities

|

|

|

$11,137

|

|

|

$13,891

|

|

|

$13,844

|

|

Total equity

|

|

|

$12,898

|

|

|

$9,914

|

|

|

$9,203

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

Historical

|

||||||||||||

|

(In millions)

|

|

|

Nine Months Ended

September 30,

|

|

|

Fiscal Year Ended

December 31,

|

|||||||||

|

|

2025

|

|

|

2024

|

|

|

2024

|

|

|

2023

|

|

|

2022

|

||

|

|

(Unaudited)

|

|

|

(Audited)

|

|||||||||||

|

Net cash provided by operating activities

|

|

|

$404

|

|

|

$555

|

|

|

$2,282

|

|

|

$2,036

|

|

|

$1,988

|

|

Net cash used in investing activities

|

|

|

$(211)

|

|

|

$(856)

|

|

|

$(1,208)

|

|

|

$(2,025)

|

|

|

$(2,521)

|

|

Net cash (used in) provided by financing activities

|

|

|

$(978)

|

|

|

$(374)

|

|

|

$(537)

|

|

|

$734

|

|

|

$497

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

•

|

greater strategic focus of financial resources and management’s efforts;

|

|

•

|

direct and differentiated access to capital resources;

|

|

•

|

value creation by offering separate investment opportunities;

|

|

•

|

improved ability to use stock as an acquisition currency; and

|

|

•

|

improved management incentive tools.

|

|

•

|

requiring a substantial portion of our cash flow from operations to make interest payments on this debt;

|

|

•

|

making it more difficult for us to satisfy debt and other obligations;

|

|

•

|

increasing the risk of a future credit ratings downgrade of our debt, which could increase future debt costs and limit the

future availability of debt financing;

|

|

•

|

increasing our vulnerability to general adverse economic and industry conditions;

|

|

•

|

reducing the cash flow available to fund capital expenditures and grow our business;

|

|

•

|

limiting our flexibility in planning for, or reacting to, changes in our business and industry; and

|

|

•

|

placing us at a competitive disadvantage relative to our competitors that may not be as highly leveraged with debt; and

|

|

•

|

the effect of political, economic and market conditions and geopolitical events;

|

|

•

|

the logistical and other challenges inherent in our operations;

|

|

•

|

the actions and initiatives of current and potential competitors;

|

|

•

|

the level and volatility of, interest rates and other market indices;

|

|

•

|

the ability of Amrize to maintain satisfactory credit ratings;

|

|

•

|

the outcome of pending litigation;

|

|

•

|

the impact of current, pending and future legislation and regulation;

|

|

•

|

factors related to the failure of Amrize to achieve some or all of the expected strategic benefits or opportunities

|

|

•

|

expected from the separation;

|

|

•

|

that Amrize may incur material costs and expenses as a result of the separation;

|

|

•

|

that Amrize has minimal history operating as an independent, publicly traded company;

|

|

•

|

Amrize’s obligation to indemnify Holcim pursuant to the agreements entered into connection with the separation and the risk

Holcim may not fulfill any obligations to indemnify Amrize under such agreements;

|

|

•

|

that under applicable tax law, Amrize may be liable for certain tax liabilities of Holcim following the separation if Holcim

were to fail to pay such taxes;

|

|

•

|

the fact that Amrize may receive worse commercial terms from third-parties for services it presently receives from Holcim;

|

|

•

|

the fact that certain of Amrize’s executive officers and directors may have actual or potential conflicts of interest because

of their previous positions at Holcim;

|

|

•

|

potential difficulties in maintaining relationships with key personnel;

|

|

•

|

that Amrize cannot rely on the earnings, assets or cash flow of Holcim and Holcim will not provide funds to finance Amrize’s

working capital or other cash requirements;

|

|

•

|

the impact of incurring new indebtedness;

|

|

•

|

changes in the ratings of our notes;

|

|

•

|

the lack of established trading markets for the notes;

|

|

•

|

actions we take that could affect our ability to satisfy our obligations under the notes; and

|

|

•

|

certain factors discussed elsewhere in this prospectus.

|

|

|

|

|

|

|

($ in millions)

|

|

|

As of

September 30,

2025

|

|

Cash and cash equivalents

|

|

|

$826

|

|

|

|

|

|

|

Debt

|

|

|

|

|

5-Year Revolving Credit Facility

|

|

|

—

|

|

Short-term borrowings

|

|

|

547

|

|

Current portion of long-term debt

|

|

|

332

|

|

Long-term debt

|

|

|

4,932

|

|

|

|

|

|

|

Equity

|

|

|

|

|

Common stock, par value of $0.01 per share,

680,250,615 shares authorized, 566,875,513 shares issued and 553,082,069 shares outstanding as of September 30, 2025

|

|

|

6

|

|

Additional paid-in capital

|

|

|

12,734

|

|

Retained earnings

|

|

|

601

|

|

Accumulated other comprehensive loss

|

|

|

(440)

|

|

Total Equity attributable to the Company

|

|

|

12,901

|

|

Total capitalization

|

|

|

$18,712

|

|

|

|

|

|

|

•

|

the effect of (i) the entry into the Revolving Credit Facility and the Bridge Loan, (ii) the issuance of the senior unsecured

notes under the April 2025 indenture, and (iii) the debt-for-debt exchange under the June 2025 indenture;

|

|

•

|

the impact of the transfer of certain employees who historically operated within specific corporate functions of Holcim; and

|

|

•

|

other adjustments as described in the accompanying notes to the unaudited pro forma condensed consolidated statements of

operations.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(In millions, except per share data)

|

|

|

Historical

|

|

|

Transaction

Accounting

Adjustments

|

|

|

Notes

|

|

|

Autonomous

Entity

Adjustments

|

|

|

Notes

|

|

|

Pro Forma

|

|

Revenues

|

|

|

$8,976

|

|

|

$—

|

|

|

|

|

|

$—

|

|

|

|

|

|

$8,976

|

|

Cost of revenues

|

|

|

(6,702)

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

(6,702)

|

|

Gross profit

|

|

|

2,274

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

2,274

|

|

Selling, general and administrative expenses

|

|

|

(850)

|

|

|

(8)

|

|

|

(c)

|

|

|

—

|

|

|

|

|

|

(858)

|

|

Gain on disposal of long-lived assets

|

|

|

9

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

9

|

|

Loss on impairments

|

|

|

(2)

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

(2)

|

|

Operating income

|

|

|

1,431

|

|

|

(8)

|

|

|

|

|

|

—

|

|

|

|

|

|

1,423

|

|

Interest expense, net

|

|

|

(328)

|

|

|

97

|

|

|

(a),(b)

|

|

|

—

|

|

|

|

|

|

(231)

|

|

Other non-operating income, net

|

|

|

2

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

2

|

|

Income before income tax expense and income from

equity method investments

|

|

|

1,105

|

|

|

89

|

|

|

|

|

|

—

|

|

|

|

|

|

1,194

|

|

Income tax expense

|

|

|

(226)

|

|

|

(22)

|

|

|

(d)

|

|

|

—

|

|

|

|

|

|

(248)

|

|

Income from equity method investments

|

|

|

5

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

5

|

|

Net income

|

|

|

884

|

|

|

67

|

|

|

|

|

|

—

|

|

|

|

|

|

951

|

|

Net loss attributable to noncontrolling interests

|

|

|

3

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

3

|

|

Net income attributable to the Company

|

|

|

$887

|

|

|

$67

|

|

|

|

|

|

—

|

|

|

|

|

|

$954

|

|

Unaudited pro forma earnings per share attributable

to the company:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.72(e)

|

|

Diluted

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.72(f)

|

|

Weighted-average number of shares outstanding:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

553.1(e)

|

|

Diluted

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

553.3(f)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(In millions, except per share data)

|

|

|

Historical

|

|

|

Transaction

Accounting

Adjustments

|

|

|

Notes

|

|

|

Autonomous

Entity

Adjustments

|

|

|

Notes

|

|

|

Pro Forma

|

|

Revenues

|

|

|

$11,704

|

|

|

$—

|

|

|

|

|

|

$—

|

|

|

|

|

|

$11,704

|

|

Cost of revenues

|

|

|

(8,634)

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

(8,634)

|

|

Gross profit

|

|

|

3,070

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

3,070

|

|

Selling, general and administrative expenses

|

|

|

(944)

|

|

|

(13)

|

|

|

(c)

|

|

|

—

|

|

|

|

|

|

(957)

|

|

Gain on disposal of long-lived assets

|

|

|

71

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

71

|

|

Loss on impairments

|

|

|

(2)

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

(2)

|

|

Operating income

|

|

|

2,195

|

|

|

(13)

|

|

|

|

|

|

—

|

|

|

|

|

|

2,182

|

|

Interest expense, net

|

|

|

(512)

|

|

|

205

|

|

|

(a),(b)

|

|

|

—

|

|

|

|

|

|

(307)

|

|

Other non-operating expense, net

|

|

|

(55)

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

(55)

|

|

Income before income tax expense and income from

equity method investments

|

|

|

1,628

|

|

|

192

|

|

|

|

|

|

—

|

|

|

|

|

|

1,820

|

|

Income tax expense

|

|

|

(368)

|

|

|

(47)

|

|

|

(d)

|

|

|

—

|

|

|

|

|

|

(415)

|

|

Income from equity method investments

|

|

|

13

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

13

|

|

Net income

|

|

|

1,273

|

|

|

145

|

|

|

|

|

|

—

|

|

|

|

|

|

1,418

|

|

Net loss attributable to noncontrolling interests

|

|

|

1

|

|

|

—

|

|

|

|

|

|

—

|

|

|

|

|

|

1

|

|

Net income attributable to the Company

|

|

|

$1,274

|

|

|

$145

|

|

|

|

|

|

$—

|

|

|

|

|

|

$1,419

|

|

Unaudited pro forma earnings per share attributable

to the company:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2.57(e)

|

|

Diluted

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2.57(f)

|

|

Weighted-average number of shares outstanding:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

553.1(e)

|

|

Diluted

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

553.1(f)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a)

|

In March 2025, we entered into the Revolving Credit Facility with commitments of $2.0 billion and the Bridge Loan with

commitments of $5.1 billion (which was permanently reduced to $1.7 billion on April 8, 2025). Total debt issuance costs associated with the Revolving Credit Facility and Bridge Loan are recorded in Prepaid expenses and other current

assets in our unaudited historical condensed consolidated balance sheet as of September 30, 2025. A pro forma adjustment has been recorded to Interest expense, net to reflect the impact of the amortization of the debt issuance costs

associated with the Revolving Credit Facility and Bridge Loan. This adjustment was calculated only from the beginning of the periods presented to the actual date of issuance as actual amounts of interest expense from the date of

issuance are reported within the historical condensed consolidated statements of operations. The unaudited pro forma condensed consolidated statements of operations do not reflect a drawdown of the Revolving Credit Facility because no

amount was drawn from or used in connection with the Spin-Off. The Bridge Loan was not utilized, and the commitments thereunder were terminated upon completion of the Spin-Off as the Spin-Off was consummated without a borrowing under

the Bridge Loan facility. See “Description of Other Indebtedness—Revolving Credit Facility” and “Description of Other Indebtedness—Bridge Loan Facility.”

|

|

(b)

|

Adjustment reflects estimated interest expense and amortization charges related to the Revolving Credit Facility, Bridge

Loan, senior unsecured notes under the April 2025 indenture, debt-for-debt exchange under the June 2025 indenture and settlement of historical intercompany debt repaid or contributed by Holcim as equity. Interest expense was calculated

assuming constant debt levels throughout the period. Interest expense was calculated only from the beginning of the period to the actual date of issuance as actual amounts of interest expense from the date of issuance are reported

within the historical condensed consolidated statements of operations.

|

|

|

|

|

|

|

|

|

|

(In millions)

|

|

|

For the

nine months

ended

September 30,

2025

|

|

|

For the

year ended

December 31,

2024

|

|

Interest expense on senior unsecured notes under the

April 2025 indenture

|

|

|

$(45)

|

|

|

$(169)

|

|

Amortization of discounts and deferred debt issuance

costs related to senior unsecured notes under the April 2025 indenture

|

|

|

(1)

|

|

|

(3)

|

|

Net interest expense on debt-for-debt exchange under

the June 2025 indenture

|

|

|

(29)

|

|

|

(62)

|

|

Net amortization on debt-for-debt exchange under the

June 2025 indenture

|

|

|

1

|

|

|

4

|

|

Interest expense on Revolving Credit Facility and Bridge Loan

|

|

|

—

|

|

|

(2)

|

|

Amortization of debt issuance costs related to

Revolving Credit Facility and Bridge Loan

|

|

|

—

|

|

|

(2)

|

|

Interest expense on intercompany debt repaid or

contributed by Parent as equity

|

|

|

183

|

|

|

454

|

|

Interest income on intercompany receivables offset upon Spin-Off

|

|

|

(12)

|

|

|

(15)

|

|

Total pro forma adjustment to Interest expense, net

|

|

|

$97

|

|

|

$205

|

|

|

|

|

|

|

|

|

|

(c)

|

In connection with the completion of the Spin-Off, Holcim transferred to the Company certain employees who historically

operated within specific corporate functions of Holcim. The audited historical combined statement of operations for the year ended December 31, 2024 included expense allocations for these employees. The unaudited historical condensed

consolidated statement of operations for the nine months ended September 30, 2025 included expense allocations for these employees up to the date of transfer. This adjustment reflects an incremental increase in costs of $7.9 million and

$12.9 million recorded to Selling,

|

|

(d)

|

Adjustment reflects the income tax effect of the transaction pro forma adjustments calculated using the applicable statutory

income tax rates in effect within the respective tax jurisdictions during the periods presented. The applicable tax rates could be impacted depending on many factors subsequent to the transaction and may be materially different from the

pro forma results.

|

|

(e)

|

The weighted-average number of shares used to compute pro forma basic earnings per share is 553,082,069 for the nine months

ended September 30, 2025 and the year ended December 31, 2024, which represents the number of Company Shares outstanding immediately following the Spin-Off.

|

|

(f)

|

The weighted-average number of shares used to compute pro forma diluted earnings per share is 553,337,480 for the nine months

ended September 30, 2025, which represents the number of weighted-average shares outstanding including the dilutive impact of equity awards converted from Holcim awards and granted by the Company as part of the Spin-Off. The actual

dilutive effect following the completion of the Spin-Off depended on various factors, including employees who changed employment between Holcim and the Company and the impact of Holcim and the Company’s equity-based compensation

arrangements. The weighted-average number of shares used to compute pro forma diluted earnings per share is 553,082,069 for the year ended December 31, 2024, which represents the number of Company Shares outstanding immediately

following the Spin-Off.

|

|

|

|

|

|

||||||||||||

|

|

|

|

For the nine months ended September 30, 2025

|

||||||||||||

|

(In millions, except per share data)

|

|

|

Net income

attributable

to the

company

|

|

|

Basic

earnings per

share

|

|

|

Basic

weighted-

average

number of

shares

outstanding

|

|

|

Diluted

earnings per

share

|

|

|

Diluted

weighted-

average

number of

shares

outstanding

|

|

Unaudited pro forma condensed consolidated net

income attributable to the company(1)

|

|

|

954

|

|

|

1.72

|

|

|

553.1

|

|

|

1.72

|

|

|

553.3

|

|

Management adjustments

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dis-synergies

|

|

|

(88)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax effect

|

|

|

20

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unaudited pro forma condensed consolidated net

income attributable to the company after management adjustments

|

|

|

886

|

|

|

1.60

|

|

|

553.1

|

|

|

1.60

|

|

|

553.3

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1)

|

As shown in the unaudited pro forma condensed consolidated statements of operations.

|

|

|

|

|

|

||||||||||||

|

|

|

|

For the year ended December 31, 2024

|

||||||||||||

|

(In millions, except per share data)

|

|

|

Net income

attributable

to the

company

|

|

|

Basic

earnings per

share

|

|

|

Basic

weighted-

average

number of

shares

outstanding

|

|

|

Diluted

earnings per

share

|

|

|

Diluted

weighted-

average

number of

shares

outstanding

|

|

Unaudited pro forma condensed consolidated net

income attributable to the company(1)

|

|

|

1,419

|

|

|

2.57

|

|

|

553.1

|

|

|

2.57

|

|

|

553.1

|

|

Management adjustments

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dis-synergies

|

|

|

(138)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax effect

|

|

|

31

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unaudited pro forma condensed consolidated net

income attributable to the company after management adjustments

|

|

|

1,312

|

|

|

2.37

|

|

|

553.1

|

|

|

2.37

|

|

|

553.1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1)

|

As shown in the unaudited pro forma condensed consolidated statements of operations.

|

|

•

|

Our Building Materials segment offers a range of branded solutions delivering high-quality products for a wide range of

applications across North America. Key product offerings of this segment include cement and aggregates, as well as a variety of downstream products and solutions such as ready-mix concrete, asphalt and other construction materials.

|

|

•

|

Our Building Envelope segment offers advanced roofing and wall systems, including single-ply membranes, insulation, shingles,

sheathing, waterproofing and protective coatings, along with adhesives, tapes and sealants that are critical to the application of roofing and wall systems. Our Building Envelope products are sold individually or in warranted systems

for new construction or R&R in commercial and residential projects. These products are sold either directly to contractors or through an authorized distributor or dealer network in North America.

|

|

•

|

Total revenues of $3,675 million, compared with $3,446 million in the three months ended September 30, 2024;

|

|

•

|

Net income of $543 million, compared with $552 million in the three months ended September 30, 2024;

|

|

•

|

Net income margin of 14.8%, compared with 16.0% in the three months ended September 30, 2024;

|

|

•

|

Adjusted EBITDA of $1,067 million, compared with $1,103 million in the three months ended September 30, 2024; and

|

|

•

|

Adjusted EBITDA Margin of 29.0%, compared with 32.0% in the three months ended September 30, 2024.

|

|

•

|

Total revenues of $8,976 million, compared with $8,855 million in the nine months ended September 30, 2024;

|

|

•

|

Net income of $884 million, compared with $981 million in the nine months ended September 30, 2024;

|

|

•

|

Net income margin of 9.8%, compared with 11.1% in the nine months ended September 30, 2024;

|

|

•

|

Adjusted EBITDA of $2,228 million, compared with $2,390 million in the nine months ended September 30, 2024;

|

|

•

|

Adjusted EBITDA Margin of 24.8%, compared with 27.0% in the nine months ended September 30, 2024; and

|

|

•

|

Cash flows provided by operating activities of $404 million, compared with $555 million in the nine months ended

September 30, 2024.

|

|

•

|

Total revenues of $11,704 million, compared with $11,677 million in 2023 and $10,726 million in 2022;

|

|

•

|

Net income of $1,273 million, compared with $955 million in 2023 and $1,107 million in 2022;

|

|

•

|

Net income margin of 10.9%, compared with 8.2% in 2023 and 10.3% in 2022;

|

|

•

|

Adjusted EBITDA of $3,181 million, compared with $2,844 million in 2023 and $2,599 million in 2022;

|

|

•

|

Adjusted EBITDA Margin of 27.2%, compared with 24.4% in 2023 and 24.2% in 2022; and

|

|

•

|

Cash flows from operating activities of $2,282 million, compared with $2,036 million in 2023 and $1,988 million in 2022.

|

|

•

|

We completed one acquisition in the three months ended September 30, 2025, compared with one acquisition in the three months

ended September 30, 2024;

|

|

•

|

We completed three acquisitions in the nine months ended September 30, 2025 for total cash consideration, net of cash

acquired, of $86 million, compared with one acquisition in the nine months ended September 30, 2024 for total cash consideration, net of cash acquired, of $21 million;

|

|

•

|

We invested $185 million in capital expenditure projects in the three months ended September 30, 2025, compared with $221

million in the three months ended September 30, 2024;

|

|

•

|

We invested $631 million in capital expenditure projects in the nine months ended September 30, 2025, compared with

$558 million in the nine months ended September 30, 2024;

|

|

•

|

We completed two acquisitions in 2024, five acquisitions in 2023 and nine acquisitions in 2022 for total cash consideration,

net of cash acquired, of $249 million, $1,607 million and $2,033 million, respectively; and

|

|

•

|

We invested $642 million in capital expenditure projects in 2024, compared with $630 million and $488 million in 2023 and

2022, respectively.

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

For the three months ended

September 30,

|

|

|

For the nine months ended

September 30,

|

||||||||||||

|

(In millions, except for percentage data)

|

|

|

2025

|

|

|

2024

|

|

|

%

change

|

|

|

2025

|

|

|

2024

|

|

|

%

change

|

|

Revenues

|

|

|

$3,675

|

|

|

$3,446

|

|

|

6.6%

|

|

|

$8,976

|

|

|

$8,855

|

|

|

1.4%

|

|

Cost of revenues

|

|

|

(2,589)

|

|

|

(2,404)

|

|

|

7.7%

|

|

|

(6,702)

|

|

|

(6,562)

|

|

|

2.1%

|

|

Gross profit

|

|

|

1,086

|

|

|

1,042

|

|

|

4.2%

|

|

|

2,274

|

|

|

2,293

|

|

|

(0.8)%

|

|

Selling, general and administrative expenses

|

|

|

(312)

|

|

|

(241)

|

|

|

29.5%

|

|